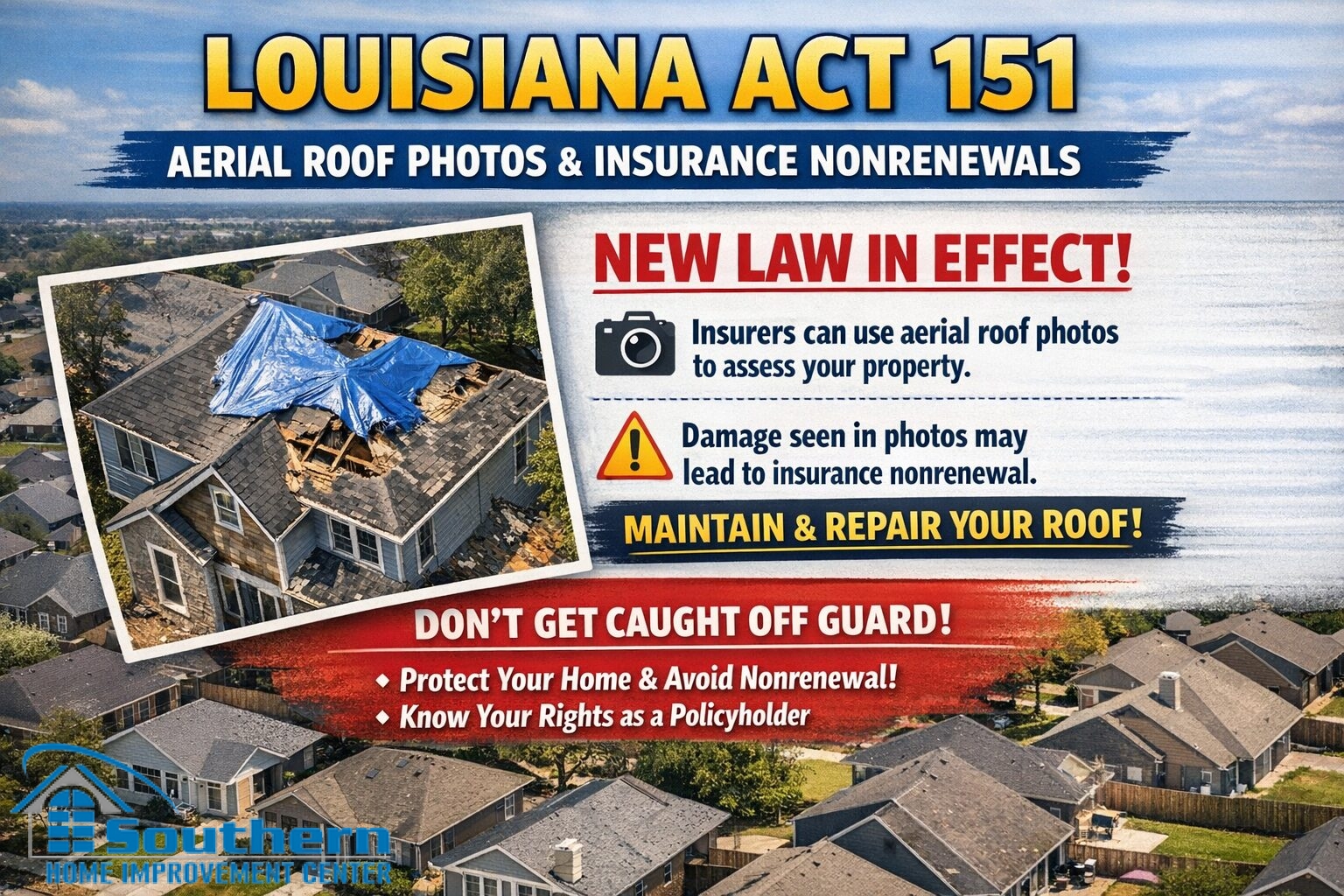

Louisiana Act 151 (SB 242): What Homeowners Should Know About Insurance Nonrenewals Based on Aerial Roof Photos

If you’ve received a homeowners insurance nonrenewal notice — or a request to “prove roof condition” — you’re not alone. Across the Gulf Coast, insurers increasingly use aerial imagery (including satellite photos) as part of underwriting and renewal reviews. In Louisiana, a state law added a specific guardrail on how aerial images can be used when a carrier is canceling or nonrenewing a homeowners policy.

This article explains what Louisiana Act 151 (SB 242) says in plain English, what it does and does not mean for homeowners, and what steps typically help you respond quickly and cleanly. This is general information, not legal advice.

What Louisiana Act 151 Actually Changed

Act 151 created Louisiana Revised Statute R.S. 22:1339, which addresses how insurers may use aerial images when identifying the specific condition that becomes the basis for cancellation or nonrenewal of a homeowners insurance policy.

- No “sole reliance” on older aerial images: An insurer shall not solely rely on aerial images to identify the specific condition behind cancellation or nonrenewal unless the images were taken within 24 months of the cancellation or nonrenewal date.

- Images can still be used for identification or location: Images used only to identify or locate the property (and improvements) may be used without an age limitation.

- Broad definition of “aerial images”: The definition includes images captured from aircraft or other airborne platforms, including satellites.

- Effective date: The act is effective May 22, 2024.

The practical takeaway is straightforward: this is not a ban on aerial images. It limits “sole reliance” on aerial images older than 24 months when the image is being used to identify the specific condition that becomes the basis for cancellation or nonrenewal.

What This Does Not Mean

Practice shows the most effective approach is to treat the law as a documentation framework — not a shortcut — and build a clean, photo-supported response:

- The law does not prevent insurers from using aerial imagery as one input in a broader decision.

- The law does not guarantee renewal.

- The law does not replace policy terms, underwriting guidelines, or other evidence an insurer may use.

A strong response still comes down to clear documentation of actual roof conditions, with current photos and a simple summary that your agent and carrier can review.

Why Roofs Get Flagged From Above

Aerial reviews can be helpful, but they can also be incomplete. Some common reasons roofs get flagged include discoloration that reads like wear, debris that looks like damage, heavy tree cover that hides details, and imagery that’s unclear or not current.

Whether the flag is accurate or not, the fastest way forward is usually the same: confirm what the carrier is claiming, confirm the date of the imagery, then document the roof condition with current, on-site photos.

What To Do If You Receive a Nonrenewal Notice Citing Roof Condition

Practice shows homeowners move faster — and waste less time — when the response is handled in a simple order:

- Ask for the specific reason in writing. Request the exact roof condition being cited (for example: “missing shingles,” “granule loss,” “visible deterioration,” or “storm damage”).

- Request the aerial image date and a copy of the image. If aerial imagery is part of the basis, ask when the photo was taken and request a copy when available.

- Schedule an on-site roof condition inspection. Get current photo documentation that clearly shows slopes, penetrations, valleys, flashing areas, and any visible deterioration or storm-related issues.

- Address true leak-risk items first. If there are repairable issues, fix them promptly and document the before/after with photos and receipts.

- Send a clean documentation packet back through your agent. Keep it simple: current photos, a short condition summary, and proof of repairs (if any). Keep copies for your records.

When the conversation stays focused on verifiable roof condition and clear timelines, it’s typically easier for an agent and carrier to review your file and decide what happens next.

When a Roof Condition Report Helps Most

A roof condition report is most useful when you need to replace assumptions with documented facts: what was inspected, what was found, and what (if anything) should be addressed next. That documentation is often helpful when a renewal decision is moving quickly and you need a clear record of current conditions.

If you need photo-supported roof documentation for an insurance renewal decision, you can learn more about our process here: Roof Certification Letter & Roof Condition Report.

FAQ

Is Act 151 the same as “insurers can’t use satellite photos”?

No. The statute addresses sole reliance on aerial images to identify the specific condition behind a cancellation or nonrenewal, and it applies a 24-month window for that use case. Images used only for identification or location of the property can be used without an age limitation.

Does Act 151 apply to roof inspections for a new policy?

R.S. 22:1339 is written around cancellation or nonrenewal of a homeowners policy. If you are shopping for a new policy, carriers may still request roof information and documentation as part of underwriting.

What if the roof is fine but the notice says otherwise?

Your goal is to replace debate with documentation. Ask what condition is being cited, confirm the image date, and provide current, on-site photo documentation that clearly shows roof condition and drainage details.

Can you guarantee my policy will be renewed?

No. Underwriting decisions are made by the insurer. A documented, photo-supported report simply gives your agent and carrier clear information to review.

If you received a roof-related nonrenewal notice in Louisiana, or you need current photo documentation to support an insurance renewal decision, contact Southern Home Improvement Center (SHIC) to schedule an inspection and request a roof condition report. Call (985) 643-6611 or (225) 766-4244 and the SHIC team will help you document roof condition and identify the most practical next step based on what is actually visible on the roof.

Reference links: Act 151 (SB 242) text and Act 151 digest.