Mississippi Windpool +16%: What to Do Before You Renew Your Policy

A rate change is never the moment you want to “wing it” with paperwork. After the Mississippi windpool rate increase took effect on January 1, 2026, many coastal homeowners started seeing renewal quotes move up. If your Mississippi windpool renewal is coming up, the fastest way to protect your options is to prepare a clean, documented file before your agent re-shops or reissues coverage.

This guide explains what the Mississippi windpool is, why the +16% matters at renewal, and what to do in the 30–60 days before your Mississippi windpool policy expires. It is general information (not insurance advice). Always confirm details with your licensed Mississippi agent.

What the Mississippi Windpool Actually Covers

The Mississippi windpool is the Mississippi Windstorm Underwriting Association (MWUA). It is designed to provide windstorm and hail coverage in specific coastal counties when the voluntary market will not write the risk. The Mississippi windpool covers wind and hail perils only, so homeowners typically still need separate coverage for other perils (and flood coverage, where applicable).

MWUA eligibility is county-based. If you are in George, Hancock, Harrison, Jackson, Pearl River, or Stone County, you may be eligible for a Mississippi windpool policy through a Mississippi licensed resident agent.

Why a +16% Increase Hits at Renewal

Even if the headline number is “+16%,” your actual premium can move more or less depending on dwelling characteristics, deductibles, endorsements, and whether your file contains current mitigation documentation. In practice, Mississippi windpool renewals are often slowed down by missing or outdated roof documentation, unclear roof age, or incomplete wind mitigation forms.

The goal is simple: when your Mississippi windpool renewal notice arrives, you want your agent to have everything needed to confirm rating details and apply any eligible credits without a back-and-forth email chain.

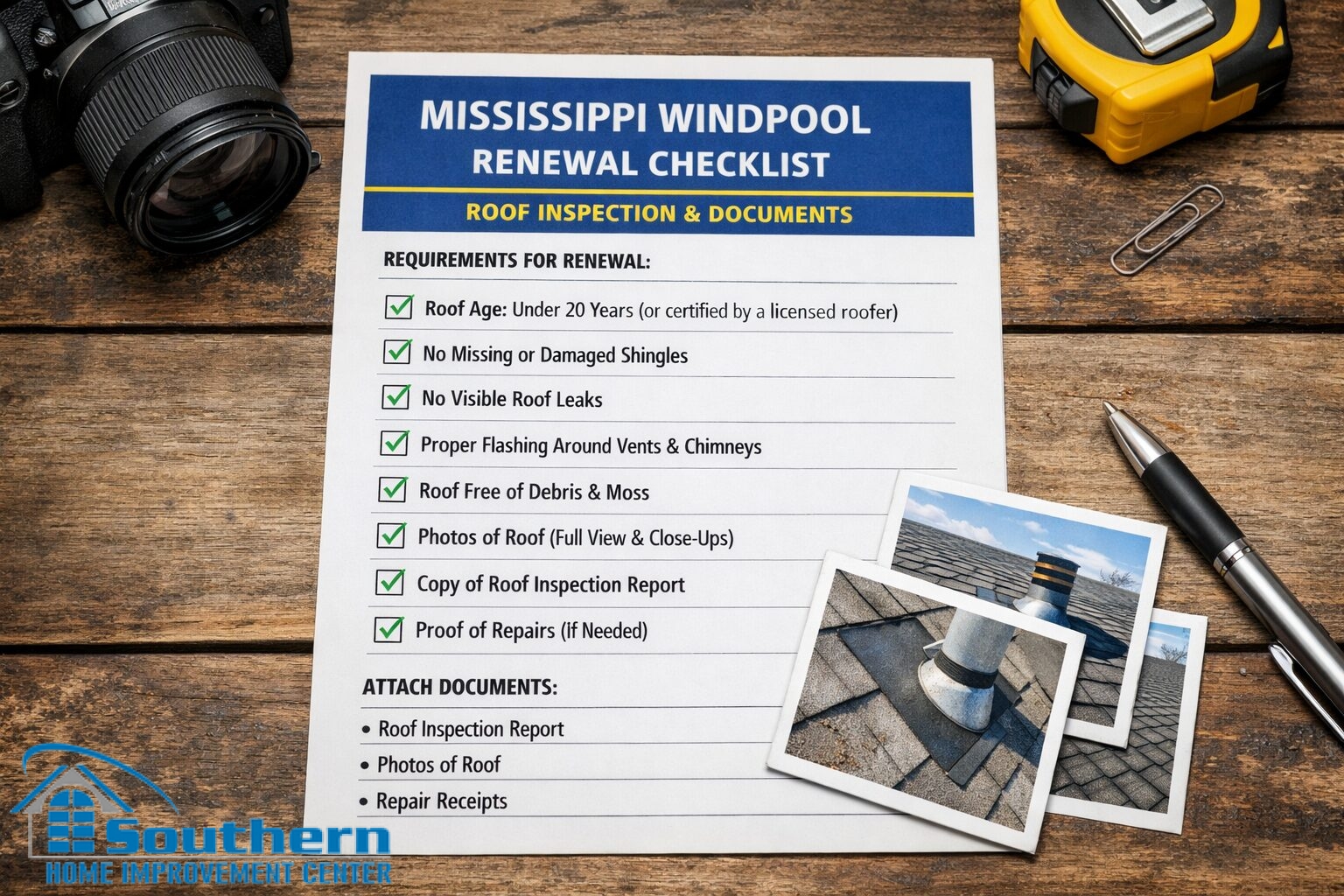

30–60 Days Before Renewal: A Mississippi Windpool Checklist

Start with actions that remove uncertainty for underwriting. These steps are boring, but they are the exact items that keep a Mississippi windpool renewal from turning into a last-minute scramble:

- Request your renewal quote early and ask your agent what documents are needed to apply mitigation credits for your Mississippi windpool policy.

- Confirm roof age and roof type (shingle vs. metal), and correct any errors on your current Mississippi windpool declarations page.

- Schedule a roof condition inspection if your roof is older, shows visible wear, or has had recent leaks. Insurers often want a current condition report at renewal.

- Gather photos of roof planes, flashings, valleys, penetrations, attic ventilation, and any prior repairs—organized by date.

- Pull prior permits, invoices, and warranties for reroofs, repairs, or opening protection upgrades that affect your Mississippi windpool rating.

- Ask about wind mitigation documentation (and whether your agent needs an updated form to support credits on your Mississippi windpool policy).

- Fix small roof issues now (loose flashings, missing seals, damaged boots) so a minor defect does not become an underwriting objection at Mississippi windpool renewal time.

Once these basics are handled, you can decide whether you are simply renewing your Mississippi windpool coverage as-is—or using renewal as the trigger to harden the house and pursue documented credits.

Upgrades That Can Support Credits (Documented, Not “Promised”)

Credits depend on program rules and documentation, not on verbal claims. MWUA publishes wind mitigation guidance and lists premium credit programs, including community building code effectiveness credits and individual risk credits tied to verified construction details. For many homeowners, the roof system is the highest-impact place to start for a Mississippi windpool strategy because it affects leak risk and wind resistance.

These are common upgrade paths homeowners discuss with their contractor and agent before a Mississippi windpool renewal:

- FORTIFIED Roof documentation (roof-level certification) when feasible, because it creates a clear, standardized record of roof-system upgrades.

- Secondary water barrier / sealed roof deck to reduce wind-driven rain intrusion after shingle loss.

- Enhanced deck attachment (verified fastening pattern) during reroofing.

- Edge securement and proper drip edge detailing, which matters in Gulf Coast wind events.

- Opening protection upgrades (impact-rated windows/doors or rated shutters) where applicable and properly documented.

The practical takeaway: if you want credits reflected on a Mississippi windpool renewal, plan upgrades early enough that you can deliver the final certificate, photos, and invoices before the renewal date.

What to Send Your Agent Before Your Mississippi Windpool Renewal

A clean packet saves time. Instead of sending random screenshots, build a single folder (or PDF) that makes it easy for your agent to confirm what changed and when. For a Mississippi windpool review, include:

- Roof install date (or best supported estimate) and the installer invoice/permit, if available.

- Roof type, product name, and manufacturer data sheets if the system was recently upgraded.

- Photo set showing sealed deck, fasteners, edge details, flashings, and final roof condition.

- Any wind mitigation form(s) your agent requests for Mississippi windpool credits.

- FORTIFIED certificate and evaluator documents if you pursued certification.

If you want a structured template, use our internal guide: FORTIFIED Roof Insurance Discount Packet. If you need a condition report specifically for renewal, see: Roof Certification Letter / Roof Condition Report.

Common Renewal Mistakes That Cost Time (and Options)

Most problems happen because the file is unclear, not because the house is “uninsurable.” Before your Mississippi windpool renewal date, avoid these avoidable issues:

- Waiting until the renewal notice arrives to schedule inspections or gather documentation.

- Assuming a discount “automatically applies” without submitting the required proof.

- Submitting photos with no labels, dates, or explanation of what the image shows.

- Letting minor roof leaks linger into renewal season—underwriting will notice.

- Changing deductibles or endorsements without understanding how it changes your Mississippi windpool premium.

Done right, renewal prep makes your agent’s job easier and keeps your Mississippi windpool renewal from turning into a deadline-driven decision.

FAQ

Is the Mississippi windpool the same as homeowners insurance?

No. The Mississippi windpool (MWUA) is windstorm and hail coverage. Homeowners typically need other coverage for additional perils, plus separate flood coverage where required.

Does MWUA renew policies automatically?

No. MWUA states that a notice of expiration and renewal quotation is sent prior to the policy expiration date. Treat your Mississippi windpool renewal as an active process and start early.

Which counties can use the Mississippi windpool?

MWUA lists eligible counties as George, Hancock, Harrison, Jackson, Pearl River, and Stone.

Will a roof upgrade guarantee a lower Mississippi windpool premium?

No. Credits depend on program rules and documentation. Upgrades can improve eligibility for credits, but your agent must confirm how the change affects your specific Mississippi windpool policy.

What should I do first if my renewal is soon?

Ask your agent what documentation is missing from your file, then schedule a roof condition inspection and organize your mitigation documents so your Mississippi windpool renewal review is fast and clean.

Get a Documented Roof Review Before Renewal

If you need a documented roof condition report or a reroof plan that supports mitigation documentation, Southern Home Improvement Center (SHIC) serves the Mississippi Gulf Coast. Call (228) 467-7484 to schedule an on-site visit and get a clear scope for repair vs. replacement.