Louisiana Citizens Rate Change 2026 — What Homeowners Should Check Before Renewal

Louisiana Citizens Property Insurance Corporation announced that personal lines rates are changing for both new and renewal business, effective January 1, 2026. Your renewal outcome can still vary widely based on plan, territory, and policy details, so the most practical approach is to confirm the official reference and then review your renewal packet with a prevention mindset.

Key takeaways: Louisiana Citizens updated personal lines rates for new and renewal policies effective January 1, 2026. Your premium change can vary by plan, territory, and policy details, so the smartest move is to review your renewal packet line by line and document your roof’s current condition. A short, photo-backed roof assessment before storm season helps reduce water-intrusion risk and keeps renewal conversations clear and specific.

For the official notice and the rate reference document, start here: 01/01/2026 Personal Lines Rate Change and Rate Level Changes Personal Lines Policies (PDF).

What Louisiana Citizens announced for January 1, 2026

The headline is simple, but the way it appears on your renewal is not. Keep the following points in mind as you review your documents and speak with your agent.

- Effective date: policies effective on or after January 1, 2026 are priced using the updated personal lines rates.

- Applies to new and renewal business: the update is not limited to new quotes.

- Rate outcomes vary: plan type, territory, and policy variables influence your final premium.

Once you confirm the effective date and the correct plan category for your policy, you can focus on the controllable part of the equation: reducing preventable water-intrusion risk and documenting roof condition clearly before the next heavy-weather window.

Why your renewal premium may not match the “overall” number

Most homeowners experience renewals as a bottom-line number, but underwriting and pricing are built from many components. Even when a statewide summary exists, your premium can move differently because of territory factors, deductibles, endorsements, and the specific characteristics of your home and roof system.

Use your renewal packet to verify the basics first: the policy form, deductibles (especially wind/hail), coverage limits, and any endorsements. Then look for what changed from the prior term. If something looks unfamiliar, ask your agent to confirm whether it is a rate update, a coverage change, or a reclassification based on inspection or third-party data.

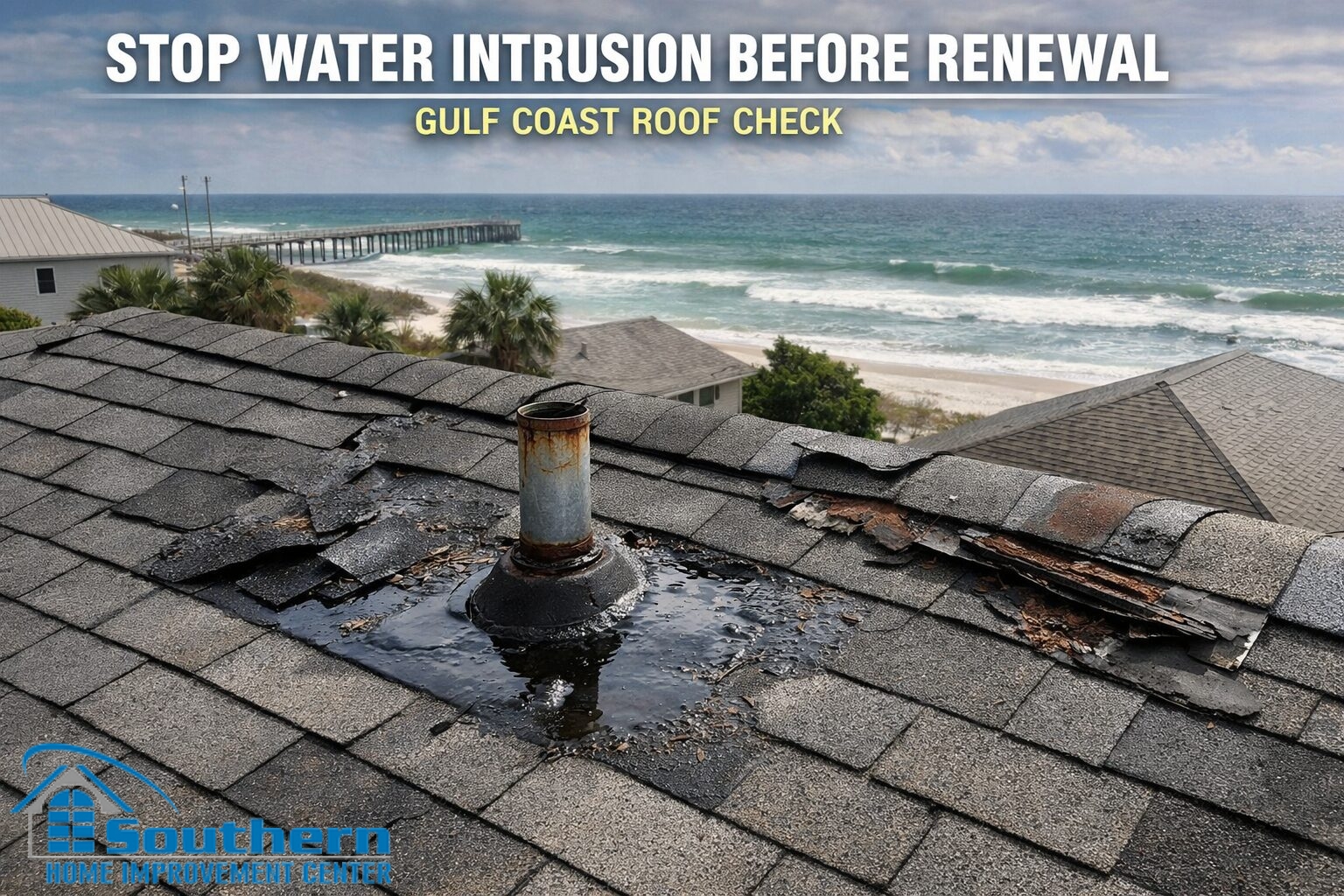

Gulf Coast reality: water intrusion is the claim driver most homeowners underestimate

Across Southeast Louisiana and the Mississippi Gulf Coast, the most expensive losses often start as small, fixable problems: a flashing gap at a roof-to-wall transition, a worn pipe boot, a valley detail that backs up during a downpour, or gutter overflow that repeatedly saturates fascia and trim. Humidity then keeps materials wet long enough for damage to spread beyond the original entry point.

If you want a quick, practical list of common pathways, see our guide: 5 Gulf Coast Water Damage Risks Homeowners Miss. It is a useful pre-renewal read because it highlights issues that do not always show up as “storm damage,” but still lead to costly interior repairs.

Pre-renewal checklist: what to document before storm season

Before your renewal date, a short, well-documented roof check can prevent weeks of back-and-forth later. The goal is not to “prove perfection,” but to create a clear baseline and catch small water-control failures early.

- Ceiling stains and attic moisture: confirm whether stains are active or historical and identify the likely entry zone.

- Flashings and transitions: roof-to-wall details, chimneys, skylights, step flashing zones, and counterflashing condition.

- Penetrations: pipe boots, vents, and sealant condition around high-risk penetrations.

- Valleys and dead zones: areas that hold debris or funnel runoff during heavy rain.

- Gutters and drainage: overflow points, downspout discharge, and fascia exposure from repeated saturation.

- Ventilation pathways: confirm intake/exhaust balance and avoid moisture buildup; see our attic ventilation guide.

- Photo set and repair receipts: a simple photo log plus invoices helps you explain what was repaired and when.

When you document these items consistently, you reduce the chance that a minor leak becomes a major interior project, and you also make renewal conversations easier because you can describe condition and scope with specifics rather than assumptions.

When a repair is enough — and when replacement is the smarter insurance play

Not every roof concern calls for replacement, but repeated water intrusion and broad wear patterns rarely get better over time. A clean decision framework helps homeowners avoid “patch fatigue” and prevents recurring interior damage.

When targeted roof repair is often sufficient

Localized issues such as a failed pipe boot, isolated flashing failure, a small wind-lift area, or a single trouble valley can often be corrected with a focused repair — especially when the surrounding shingles are still in good condition and the roof is not near end-of-life.

When replacement is usually the safer long-term decision

If the roof shows widespread brittleness, repeated leaks in different zones, chronic valley problems, failing flashings across multiple transitions, or aging shingles that no longer seal reliably, replacement often becomes the more cost-effective path. If you are weighing options, start with our overview of roof replacement & installation to compare scope, timelines, and typical decision points.

FORTIFIED, discounts, and paperwork: how to keep the conversation clean

Some homeowners explore resilience upgrades as part of renewal planning. If you are considering a documentation-forward approach, review our program overview for certified FORTIFIED roof installation and the insurer-ready FORTIFIED roof discount packet page. Every carrier handles incentives differently, so the best practice is to confirm requirements with your agent once your scope is defined and documentation expectations are clear.

If you are also evaluating grant eligibility, see our overview of the Louisiana Fortify Homes Program and bring your questions to the inspection visit so your scope and documentation plan can align with your timing.

FAQs

When do the Louisiana Citizens personal lines rate changes take effect?

Louisiana Citizens states that personal lines rates are changing for new and renewal business effective January 1, 2026. The official notice and reference document are linked above so you can confirm the effective date for your specific policy type.

Do the new rates apply to renewals as well as new policies?

Yes. Louisiana Citizens’ notice indicates the change applies to both new and renewal business. Your premium still depends on plan, territory, and policy details, so use your renewal packet to confirm what changed.

Why can two homeowners see very different renewal outcomes?

Even under the same announcement, premiums vary based on territory, deductibles, endorsements, coverage limits, and the characteristics of the home and roof system. Ask your agent to clarify whether a change is rate-driven, coverage-driven, or tied to updated property data.

What is the fastest way to reduce water-damage risk before storm season?

Start with a roof inspection that focuses on water-control details: flashings, penetrations, valleys, gutter overflow points, and attic moisture conditions. Catching small failures early prevents expensive interior repairs in high-humidity climates.

Should I repair or replace if I’m seeing recurring leaks?

Localized failures can often be repaired, but recurring leaks across multiple zones, widespread shingle wear, and repeated interior staining are strong signals that replacement may be the safer long-term decision. A documented assessment makes the decision clearer.

Does a FORTIFIED roof automatically lower premiums?

Discount and incentive rules vary by carrier and policy. If you are considering a documentation-forward resilience upgrade, confirm requirements with your agent and use a scope that supports clean documentation and recordkeeping.

If you want a documented roof assessment and a clear, itemized scope for Southeast Louisiana or the Mississippi Gulf Coast, contact Southern Home Improvement Center (SHIC) to schedule an inspection — call (225) 766-4244 (Baton Rouge) or (985) 643-6611 (Slidell/Northshore).