Louisiana Named-Storm Deductible Explained — What You’ll Actually Pay for Roof Damage

A named-storm deductible is not the same as your standard homeowners deductible. In Louisiana, it can be a separate deductible that applies only when roof damage is tied to a named storm, and it is often written as a percentage of your home’s insured value instead of a flat dollar amount.

That is why a roof claim that sounds “covered” can still leave you with a much larger out-of-pocket cost than expected. If you are starting from scratch, it helps to first understand the broader storm insurance process for roof damage in Louisiana and Mississippi before focusing on the deductible itself.

Why this matters more than most homeowners expect

After a tropical storm or hurricane, most homeowners focus on visible damage first: lifted shingles, missing tabs, ridge damage, wet ceilings, or active leaks. But the most important financial number in the first 24 to 48 hours is often the deductible, not the damage total. If your policy uses a percentage-based named-storm deductible, the amount you must absorb before coverage starts can be several thousand dollars.

That changes the decision-making immediately. Instead of asking only, “Will insurance cover this?”, the better question is, “Does the damage clearly exceed the deductible enough to make a claim worthwhile?” That is especially important if you are already comparing repair versus replacement.

For a realistic view of local pricing, homeowners often pair the deductible math with the numbers in Cost of a New Roof in Louisiana so they can see how far their out-of-pocket responsibility may actually go.

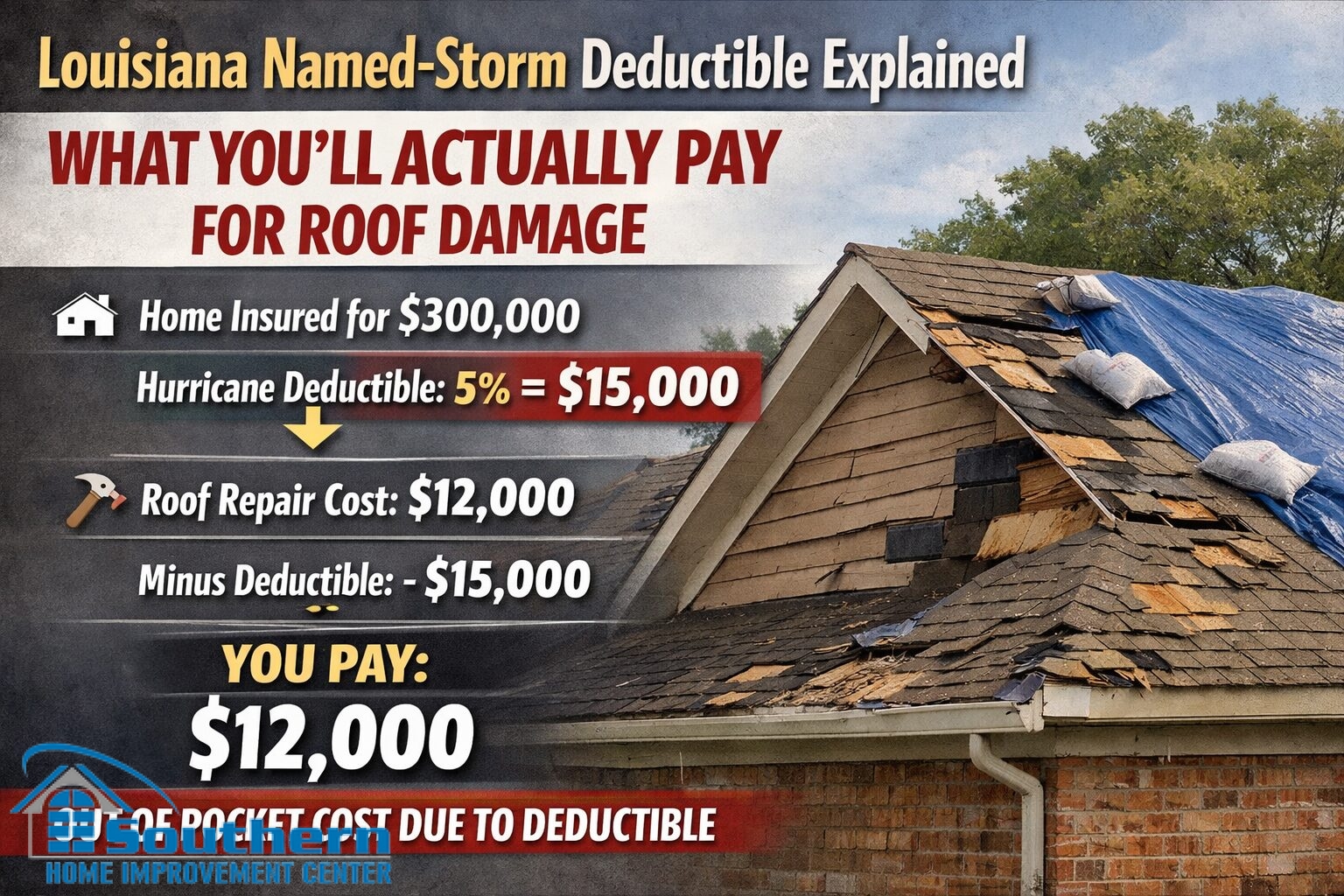

How to calculate your named-storm deductible

The fastest way to make this practical is to convert the percentage into a real dollar amount. If your named-storm deductible is 2%, 3%, or 5%, that percentage is usually applied to the insured value listed in your policy, not to the final repair invoice.

- If your home is insured for $250,000 and your named-storm deductible is 2%, your out-of-pocket amount is $5,000.

- If your home is insured for $350,000 and your named-storm deductible is 3%, your out-of-pocket amount is $10,500.

- If your home is insured for $500,000 and your named-storm deductible is 5%, your out-of-pocket amount is $25,000.

Once you see the number in dollars, the claim becomes easier to evaluate. A roof repair that lands below or near that threshold may not produce much insurance benefit even if the damage is technically covered. A full replacement or a multi-slope storm loss is a different conversation.

If you want a more complete claims workflow after the math, use Hurricane Roof Insurance Claims in Louisiana & Mississippi as the next step.

Named-storm vs. hurricane vs. wind/hail

These terms are often treated like they mean the same thing, but they do not always trigger the same deductible. A named-storm deductible may apply when the damage is tied to an officially named weather event, even if it is not a hurricane at landfall. A hurricane deductible can be narrower and tied specifically to a storm classified as a hurricane. Some policies also include a separate wind or wind/hail deductible that can apply more broadly.

The practical takeaway is simple: do not rely on memory, assumptions, or what your neighbor’s policy says. Check your declarations page and confirm which deductible applies, how it is triggered, and whether it is written as a percentage or a flat amount. One word in the policy language can change the entire financial outcome of the claim.

What to do before you file a roof claim

Before you call the carrier, slow the process down just enough to gather clean documentation. A rushed claim with poor photos and no baseline often creates more confusion than clarity. The goal is to document first, stabilize second, and then decide whether the scope justifies the deductible.

- Take clear photos of missing shingles, exposed areas, ridge lines, flashing, gutters, and any interior water staining.

- Document the attic if water intrusion is visible from inside.

- Write down the date of the storm and the date you first noticed the damage.

- Prevent additional water intrusion if it is safe to do so.

- Calculate the deductible in dollars before assuming the claim will produce meaningful payment.

If you want a cleaner system for organizing photos, receipts, and damage notes, it helps to use a repeatable checklist like Home Inventory & Storm Claim Kit. That keeps the deductible decision tied to real evidence instead of rough guesses made under stress.

When a repair may make more sense than a claim

Not every storm issue should become an insurance claim. If the damage is isolated to one section, if the shingles on the surrounding slopes are still serviceable, and if the likely repair falls at or below your deductible, paying out of pocket may be the cleaner choice. This is especially true when the claim would produce little benefit after the deductible is applied.

On the other hand, if multiple slopes are affected, if wind-driven rain reached the underlayment or decking, or if the roof was already near the end of its useful life, the economics may shift quickly. In those cases, a proper inspection becomes much more important than a quick driveway opinion.

If age is already part of the equation, review Roof Age & Insurance in Louisiana so you can see how roof condition, underwriting, and claim expectations intersect.

When an inspection is worth doing first

A roof inspection is most useful when the deductible math is unclear and the damage is not obviously minor or obviously catastrophic. That is the middle zone where homeowners make the most expensive mistakes: filing too quickly on a small scope, delaying too long on hidden damage, or underestimating how much water entered through flashing, ridge vents, valleys, or penetrations.

In that situation, the smartest move is not to guess — it is to get photo-based documentation and a clear scope first. If your insurance company is also asking for updated roof condition details, the next logical reference is 4-Point Insurance Inspection, especially if the deductible decision overlaps with renewal questions or underwriting requests.

The bottom line for Louisiana homeowners

A named-storm deductible can completely change what a “covered” roof loss actually costs you. Before filing, convert the percentage into a dollar amount, compare that number to the likely repair or replacement scope, and make the decision from there. That simple step helps you avoid filing weak claims, underestimating your out-of-pocket cost, or delaying needed work because the policy language was never translated into real numbers.

If recent storm damage has left you unsure whether you are dealing with a minor repair, a larger insurance claim, or a full reroof decision, fill out the form below with your address and a short description of what you are seeing. A clear inspection and written scope make it much easier to decide what to do next.

Get a clearer next step after storm damage

After a named storm, the biggest mistake is making a fast decision without knowing the deductible, the true scope of damage, or whether the roof issue is limited to one area or affects multiple slopes. A clear inspection, photo documentation, and a written scope help you compare repair, insurance, and replacement options with real numbers instead of guesswork.

If recent storm damage has left you unsure whether you are dealing with a minor repair, a larger insurance claim, or a full roof replacement, fill out the form below with your address and a short description of what you are seeing. Our team will review the details, help you understand the likely scope, and provide a clear next step with a free estimate.

To speak with Southern Home Improvement Center (SHIC) directly, call Slidell/Lacombe at (985) 643-6611, New Orleans/Jefferson at (504) 833-1835, Mandeville/Covington at (985) 626-3755, Baton Rouge at (225) 766-4244, Gulf Coast at (228) 467-7484, or Toll Free at (800) 650-2032.