4-Point Insurance Inspection in Louisiana & Mississippi — What It Is and How to Prepare

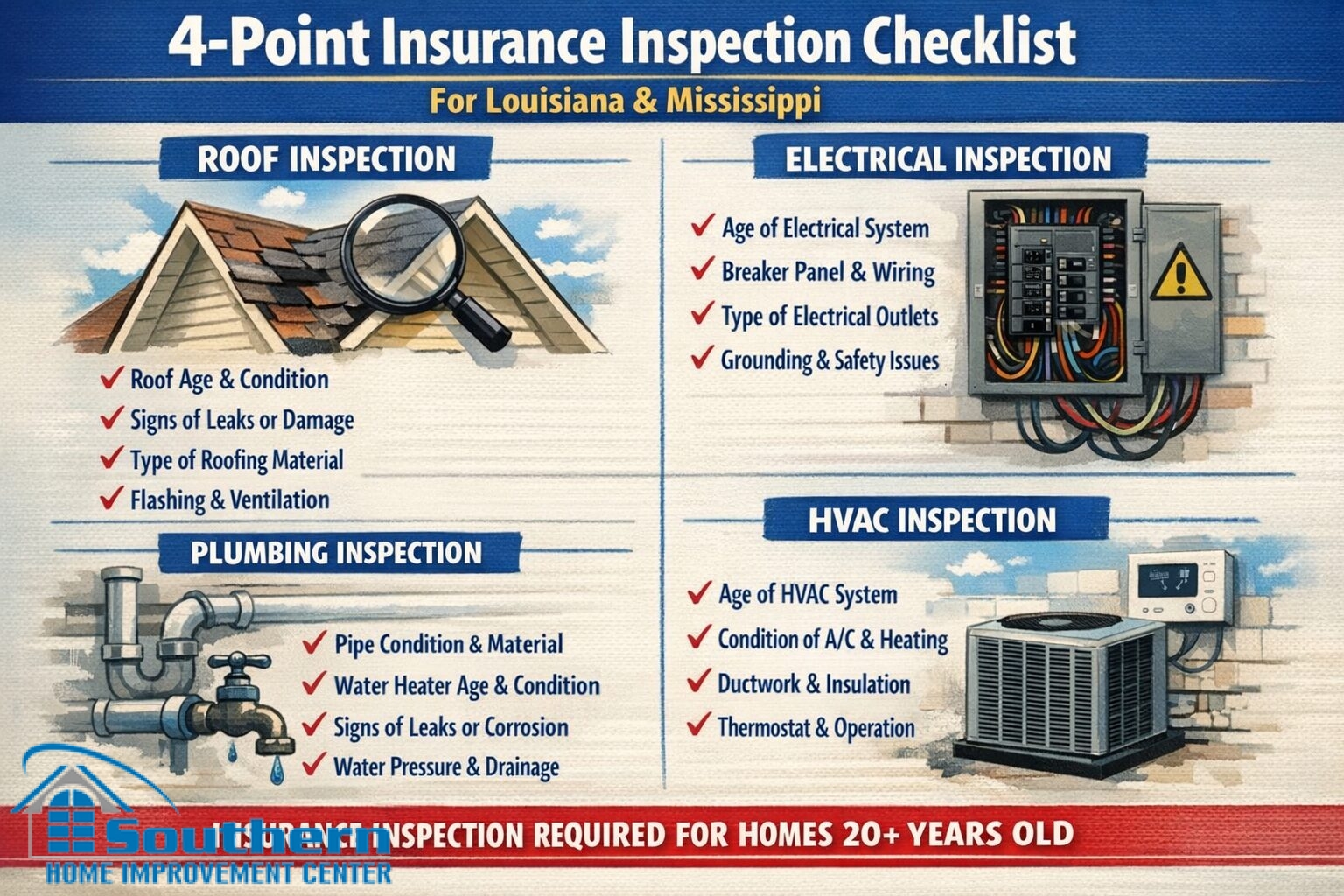

If your insurance company asks for a “4-point inspection,” you are not alone. A 4-point insurance inspection is a focused report that looks at four major systems — the roof, electrical, plumbing, and HVAC — so an insurer can understand risk on an older home or a policy renewal.

This guide explains what the inspection covers, what commonly triggers underwriting delays, and how to prepare without wasting time. Southern Home Improvement Center (SHIC) can help with the roof portion — inspection, documentation, and repair-versus-replacement options — and we can point you to the right next step for the other systems when needed.

What a 4-Point Inspection Covers

A 4-point inspection is not a full home inspection. It is a targeted insurance-oriented review of four systems insurers care about most when deciding eligibility, terms, or renewals.

- Roof — age, visible condition, active leaks, missing/damaged materials, flashing issues

- Electrical — panel type/condition, visible hazards, outdated components, basic safety concerns

- Plumbing — leaks, corrosion, pipe material, water heater basics

- HVAC — approximate age/condition, safe operation indicators, visible issues

The practical takeaway: insurers use the report to decide whether they can write the policy as-is, request repairs, exclude certain risks, or require more documentation.

Why Insurers Request It (And When It Usually Comes Up)

In many cases, the request shows up when a home is older, when a policy is being renewed, when shopping for a new carrier, or when underwriting needs clarity after a change in risk. The inspection is meant to reduce uncertainty — especially around roof condition and any obvious hazards in critical systems.

If you received a non-renewal notice or an underwriting request tied to roof age/condition, you may also be asked for a roof condition report or roof certification letter. If that’s your situation, start here: Roof Certification Letter & Roof Condition Report.

Before You Schedule — The “No-Regrets” Prep Checklist

Practice shows that most delays happen because the inspector cannot verify basics quickly (age, visible condition, access, obvious leaks), or because small issues look bigger when there is no documentation. Use this checklist first — it is fast, and it helps the inspection go smoother.

- Find any paperwork you have: permits, invoices, warranties, installation dates (roof, HVAC, water heater).

- Clear access: attic hatch, electrical panel, HVAC closet, water heater area.

- Fix obvious “presentation” issues: active drips, stained ceiling spots (even if old), loose downspouts, obvious gutter overflow paths.

- Take your own photo set (ground-level): each roof slope, problem areas, attic access area, any interior stain spots.

- Write down what you already know: roof age estimate, last repair date, known prior leaks (and whether they were corrected).

You are not trying to “hide” anything — you are trying to make the condition easy to verify and easy to document so underwriting does not pause the file.

Roof Section — What Usually Causes Problems

On Gulf Coast homes, roof findings are often the biggest driver of “repair required” notes, simply because water entry risk is expensive and urgent for insurers. The items below are common flags that can trigger follow-up questions.

- Active leaks or recent water staining that looks unresolved.

- Missing shingles/materials, lifted edges, exposed fasteners, or open penetrations.

- Flashing issues at chimneys, walls, valleys, and around vents.

- Evidence of repeated patching without a clear scope (it reads like “ongoing problem”).

- Roof age uncertainty — no documentation, no clear estimate, or conflicting info.

If you want a quick homeowner-friendly way to spot obvious issues before the inspection, use: The 15-Minute Roof & Exterior Checkup.

Documentation That Speeds Up Underwriting

Underwriting moves faster when evidence is organized. If you are dealing with a storm-related concern, or you want a “clean” documentation package, use this simple photo checklist: Documents for Insurer — 1-Page Photo Checklist.

For roof-specific needs (renewals, underwriting questions, repair vs replacement decisions), SHIC provides photo-documented roof assessments and clear next steps. If the roof portion is the sticking point, start with: Roof Damage Inspection & Insurance Documentation.

What If the Report Comes Back With “Repairs Required”?

Don’t panic — this is common, and it is usually solvable. The key is to treat the report like a punch list, fix what is reasonable, and then re-document cleanly. The fastest path is:

- Ask for clarity on the exact items that must be corrected (roof vs electrical vs plumbing vs HVAC).

- Fix items using the correct licensed trade where required (especially electrical and HVAC).

- Document the fix with photos and invoices.

- Provide the updated documentation to your agent/underwriter promptly.

Most delays come from vague scopes and missing proof — not from the existence of a punch list itself.

Frequently Asked Questions

Is a 4-point inspection the same as a full home inspection?

No. A 4-point inspection focuses only on the roof, electrical, plumbing, and HVAC for insurance risk. A full home inspection is broader and covers many more components.

Can I do a 4-point inspection myself?

Insurers typically require a report from a qualified inspector. Homeowners can prepare and document conditions, but the inspection report itself is usually completed by a professional.

What roof documentation helps the most?

A clear photo set of each slope, visible defects, flashing areas, and any interior staining — plus any invoices, permits, or warranty records you have.

Will a new roof automatically “pass” the roof portion?

A newer roof helps, but insurers still look for installation quality and signs of leaks, flashing issues, or other visible defects. Documentation and clean details matter.

If my insurer is questioning roof condition, what should I request?

Ask whether they want a roof condition report or roof certification letter and what documentation format they prefer. You can start with: Roof Certification Letter & Roof Condition Report.

Does SHIC perform the entire 4-point inspection?

SHIC can help with the roof portion — inspection, documentation, and repair-versus-replacement options — and we can guide next steps for the other systems if the report flags issues.

If you need roof documentation for insurance, or you want a clear plan before underwriting delays your renewal, contact Southern Home Improvement Center (SHIC) via our Contact page. You can also call (985) 643-6611 or (225) 766-4244 to schedule an inspection and get photo-based documentation of roof condition.