Louisiana Department of Insurance Storm Claim Guidance After the March 2026 Storms — What Homeowners Should Do First

After the March 2026 storm damage in Tangipahoa Parish and nearby areas, the Louisiana Department of Insurance issued practical claim guidance that homeowners can use right away. This update focuses on what to do first, what to document before cleanup, how temporary roof protection fits into the process, and how to screen contractors and adjusters before the situation becomes more expensive or more confusing.

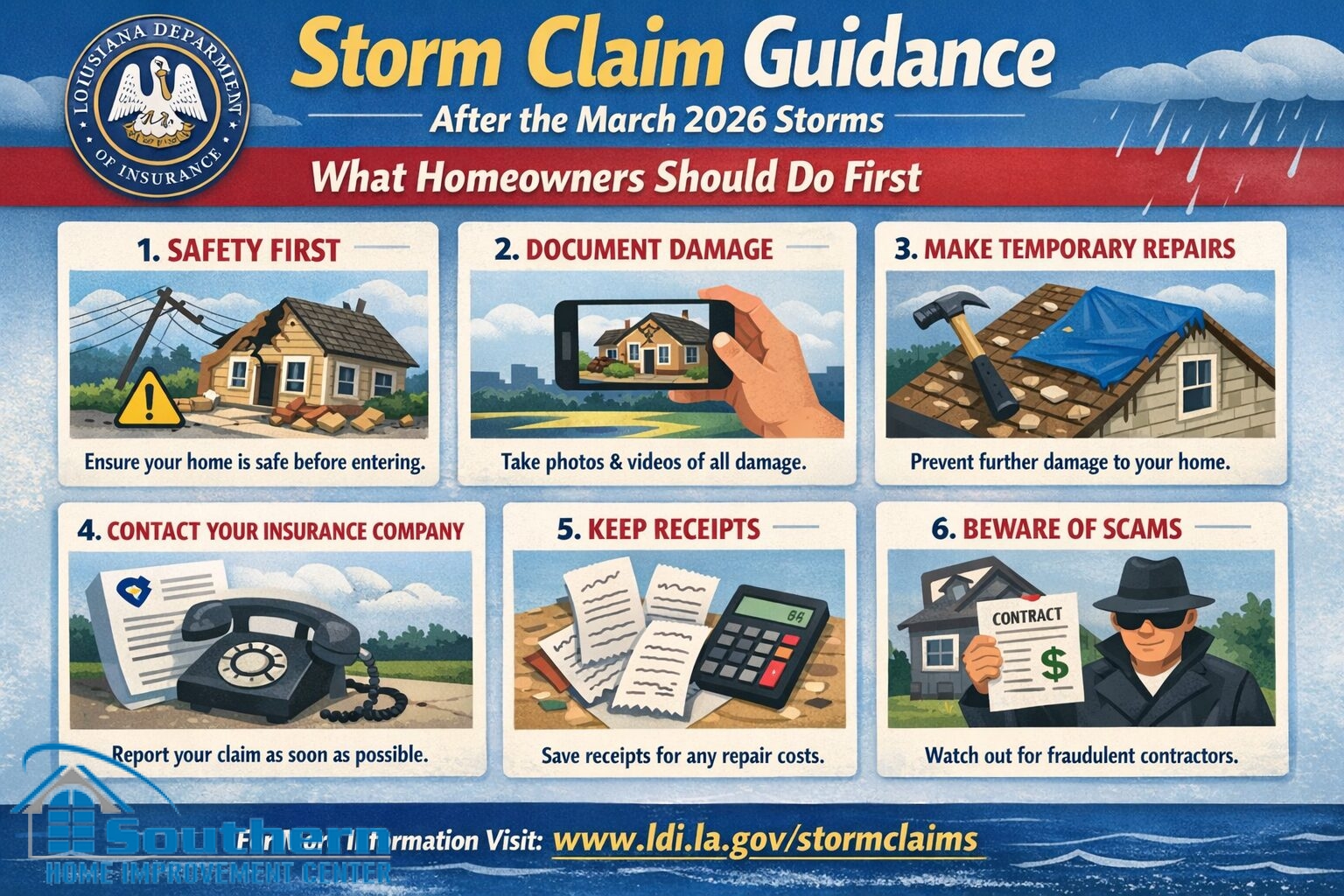

What the Louisiana Department of Insurance Told Homeowners to Do

The most useful part of the new guidance is that it does not start with a contractor sales pitch. It starts with claim discipline. According to the official March 13, 2026 Louisiana Department of Insurance release, homeowners affected by the Wednesday tornadoes and severe storms should contact their insurer or agent first, document damage before cleanup, take temporary protective measures, and verify the identity and licensure of anyone arriving at the property.

That is a strong reminder for homeowners in Southeast Louisiana because the hours right after storm damage are when pressure builds fastest. There is usually urgency, there may be active leaks, and it becomes easy to confuse emergency dry-in work with permanent repair decisions. For a broader Gulf Coast workflow after storm damage, our Storm Roof Damage & Insurance Guide — Louisiana & Mississippi breaks down what to capture, how to stabilize the home, and where documentation matters most.

Call Your Insurer First

Open the claim before assumptions harden into bad paperwork or missing steps.

Document Before Cleanup

Photos and video come first. Discarded evidence is hard to recreate later.

Mitigate Further Damage

Tarping and boarding can be necessary, but they are temporary protection, not final repair.

Verify Who Shows Up

Check IDs, licenses, and company status before authorizing work or sharing claim details.

What to Do First if Your Roof or Exterior Was Hit

Start by slowing the process down just enough to get a clean record. If your roof, siding, fascia, soffit, or gutters may have been affected, take wide shots and close shots before debris is moved. Include the roofline, any missing shingles, exposed underlayment, bent metal, lifted flashing, water entry points inside the attic, and any ceiling staining that appears after the storm. If you want a clean documentation sequence, our 1-Page Storm Claim Photo Checklist gives a practical file structure that homeowners can actually use.

The next step is triage, not guessing. If you are not sure whether the loss is limited to a few shingles or points to a bigger roof system problem, compare the situation against our March 11 Storm Damage Inspection Guide. That page is useful because it helps separate visible storm damage from hidden moisture pathways around flashing, valleys, wall transitions, and drainage components.

If the home is taking on water, the goal is not to make permanent decisions from a ladder in a panic. The goal is to protect the house, protect the claim file, and keep the project sequence organized. That is also where a written inspection record helps. Our free post-storm roof inspection page explains how a documented inspection fits between the first photos and the bigger repair-versus-replacement conversation.

Temporary Roof Protection Still Matters — But It Is Not the Whole Job

One of the most important points in the LDI guidance is the duty to mitigate further damage. In plain terms, homeowners are expected to take reasonable steps to prevent the loss from getting worse. That can mean placing a tarp over an opening, boarding a broken window, or otherwise stopping water from continuing to enter the house. The official LDI severe weather resources page is worth bookmarking because it centralizes claim help, complaints, and homeowner guidance after a storm event.

That said, temporary measures should stay temporary. Emergency dry-in is not the same thing as a final repair scope, and it should not be used to pressure a homeowner into signing broad paperwork before the damage is clearly documented. Our Emergency Roof Tarping guide explains what tarping does well, what it does not do, and why it needs to be tied to inspection photos and receipts.

If a crew is doing emergency protection, keep the invoice, the photos, and the timeline together. LDI specifically tells homeowners to keep receipts for temporary protective measures. That matters because emergency spending becomes much easier to explain when it is documented from the start instead of reconstructed later.

Good Temporary-Repair Habits

- Photograph the damage before the tarp or board-up goes on.

- Photograph the temporary protection after it is installed.

- Save receipts, invoices, and date stamps.

- Separate emergency dry-in from permanent scope discussions.

- Do not let a “same-day fix” erase the evidence your claim may need.

Who Should Be Allowed to Help — And Who Should Not

LDI’s warning about bad actors is not filler. Storms create a short window where homeowners are tired, worried, and easier to pressure. The department specifically warned that unlicensed individuals may pose as contractors or inspectors, and it advised homeowners to ask for identification and verify licensure when someone shows up at the property. For insurance-side verification, the state’s official Producer / Adjuster search is the cleanest way to confirm an adjuster or producer status. For contractor-side screening, use the official Louisiana State Licensing Board for Contractors search.

This is also the point where homeowners need to keep roles straight. A contractor documents conditions, explains repair options, and performs the work. A public adjuster handles claim representation. Those are not the same job. Our page on Contractor vs. Public Adjuster in Louisiana lays out the difference in plain language, which helps avoid the confusion that appears when storm response moves too fast.

It is also smart to screen the paperwork before you sign anything. After a storm, homeowners may be asked to sign work authorizations, contingency contracts, or broader forms before the claim path is even clear. If you want a calmer framework for that decision, review Before You Sign Storm Damage Paperwork in Louisiana and Should You Sign a Roofing Contingency Contract Before the Adjuster Visit? before the project gets more locked in than it needs to be.

What This Means for Homeowners in Tangipahoa Parish and Nearby Areas

The official guidance was issued with Tangipahoa Parish and surrounding communities in mind, but the process applies much more broadly across Louisiana after wind, hail, tornado, and severe storm losses. The sequence is simple: open the claim, preserve the evidence, stop the damage from spreading, verify the people involved, and do not let urgency erase the paper trail. For homeowners sorting through ongoing local updates, our Official Louisiana & Mississippi Homeowner Updates page is a good starting point because it pulls state-facing guidance into one place.

There is another reason this matters. The same storm that creates a claim can also create a sales environment where homeowners are told that the deductible does not matter, paperwork can wait, or licensure is secondary to “getting started.” That is exactly the kind of shortcut thinking that leads to expensive confusion later. Our recent article on deductible waiver red flags is worth reading before a storm project turns into an insurance misunderstanding.

Related SHIC Pages

These pages fit naturally with the official LDI guidance because they help homeowners move from the first claim steps into clearer documentation, safer screening, and better roof decisions.

FAQ

Should I clean up storm debris before I take photos?

Can I put a tarp on the roof before the adjuster comes?

How do I verify an adjuster or contractor in Louisiana?

Does a storm claim mean my insurer can automatically cancel my policy?

Where does SHIC fit after storm damage?

Need a Local Roof Inspection After Storm Damage?

Southern Home Improvement Center (SHIC) can document visible roof conditions, explain the likely next step in plain language, and help you separate emergency protection from larger repair or replacement decisions without pressure.